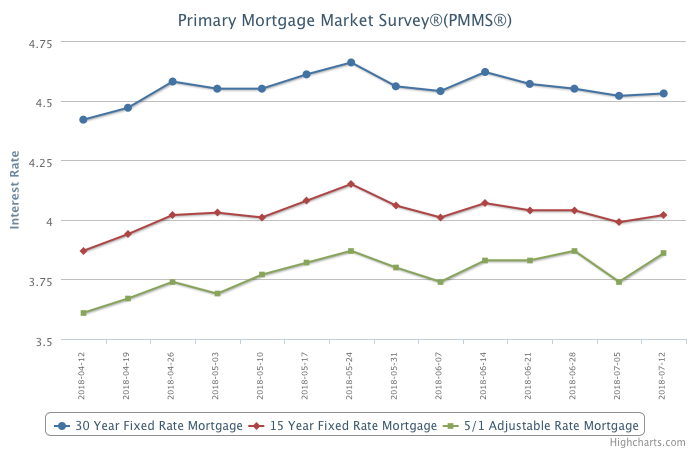

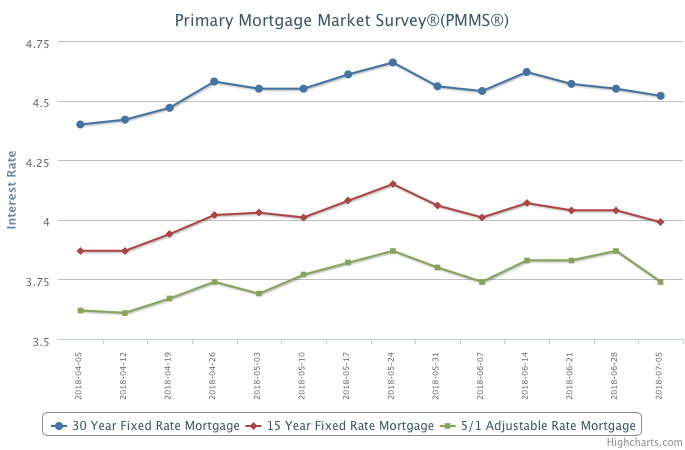

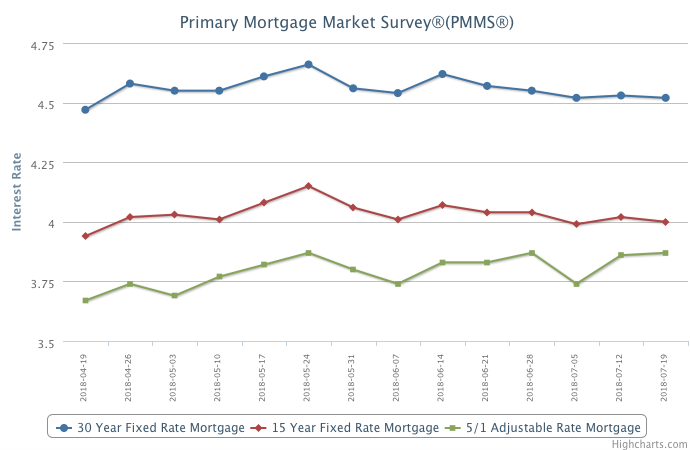

Mortgage rates were once again mostly flat over the past week, inching backward slightly.

Manufacturing output and consumer spending showed improvements, but construction activity was a disappointment. This meant there was no driving force to move mortgage rates in any meaningful way, which has been the theme in the last two months. That’s good news for price sensitive home shoppers, given that this stability in borrowing costs allows them a little extra time to find the right home.