For Week Ending August 31, 2019

For Week Ending August 31, 2019

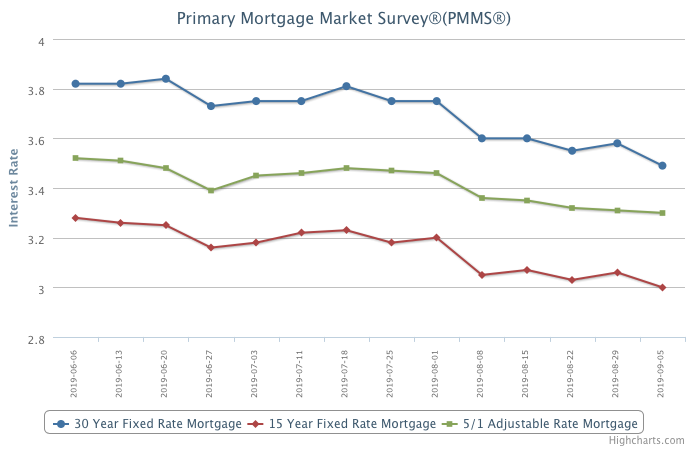

Recent mortgage rate declines may provide a small tailwind as we enter the fall housing market, giving buyers a bit more buying power and a little more incentive to lock in a home purchase. However, stock market volatility and concern of a wider economic slowdown in the coming year may temper some buyer enthusiasm. But as rents continue to rise, the value proposition of owning a home remains a compelling option and a goal of most Americans.

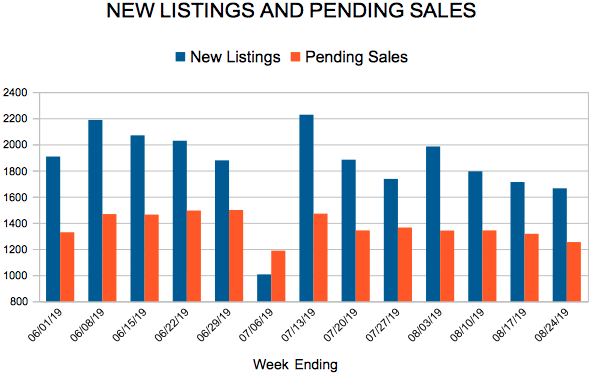

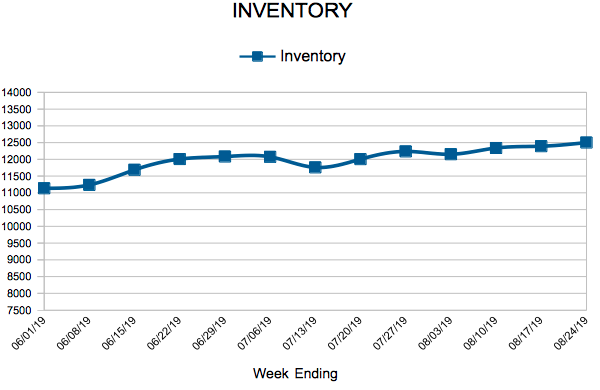

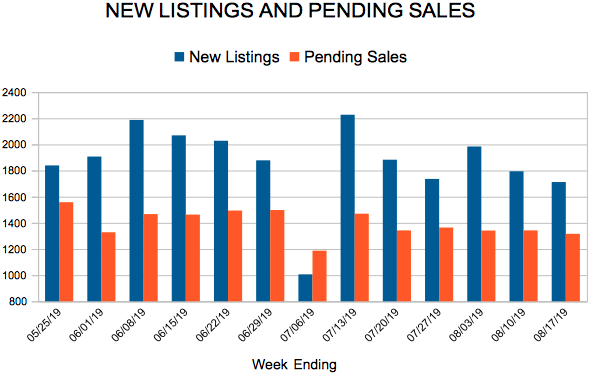

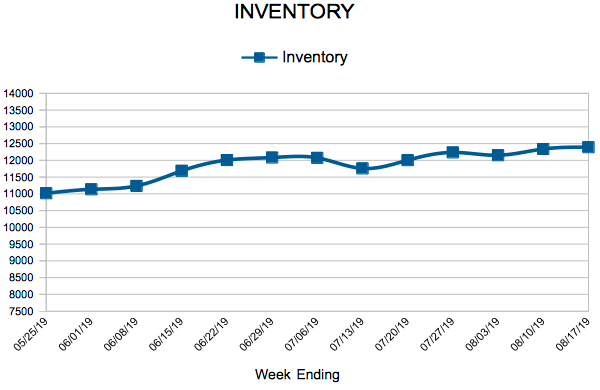

In the Twin Cities region, for the week ending August 31:

- New Listings increased 4.9% to 1,359

- Pending Sales decreased 3.1% to 1,250

- Inventory decreased 4.4% to 12,498

For the month of July:

- Median Sales Price increased 5.9% to $283,900

- Days on Market remained flat at 38

- Percent of Original List Price Received decreased 0.1% to 99.7%

- Months Supply of Homes For Sale remained flat at 2.5

All comparisons are to 2018

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.